|

Our Home Ijarah products can be tailored to suit individual needs. Switch your Self Managed Super to ICFAL and join a fund of $50 million+ that provides Shariah compliant returns on its investments. Our shariah-compliant financing solutions are here to help you to meet your property, vehicle or commercial need. I recommended all in Australia to take loan from them to buy property. An early recipient of NAB’s Islamic finance services has been Binah, a construction company in Sydney. Offering retail Islamic finance products may foster social inclusion, enabling Australian Muslims to access products that may be more consistent with their principles and beliefs. Developed in a mere six weeks, the Shariah-compliant prototype enables any financial institution to enhance their offering and into Islamic banking services through a technology stack that essentially plugs into the infrastructure. ESG — Environmental, Social, and Governance — has become the industry buzzword of 2022. However, while it all looks great on face value, customers are starting to question commitments from banks and financial institutions to not only environmental governance, but also its social counterparts. In February 2010, one of our 'big four' banks, Westpac, was the first Australian bank to offer a short-term wholesale investment product structured specifically developed for Islamic financial institutions. Islamic home loans are available for many purposes such as construction and purchasing vacant land, although they are not typically used for refinancing. They also come in full documentation and low documentation versions, depending on your leasing needs. Speaking to The Adviser on the occasion of the RADI being granted, Islamic Bank Australia chief executive Dean Gillespie outlined that the bank will look to distribute home finance through the broker channel, as well as direct. Settle Easy has updated its online platform to provide automatic updates to mortgage brokers and real estate agents during the conveyancing ... We offer an alternative solution for Muslims in an Australian landscape. With the number of Muslims in Australia growing by more than 6 per cent every year, we’re excited to be bringing this new type of banking to the Australian community,” the CEO added. Similarly, for personal finance – Islamic Bank Australia would purchase the item and then sell it to the customer. Let me assure you the Government is intent on developing Australia as a regional financial centre and it sees Islamic finance as a fundamental part of that endeavour. Businesses that offer Islamic finance products should benefit from any successes we achieve in that sphere. First, the Report recommends the removal of regulatory barriers to the development of Islamic finance products in Australia. While our finance and insurance sector already generates significant jobs and wealth, we recognise that it has a great untapped potential. This outcome provides tentative signs that a self-sustaining private sector recovery is in prospect, although growth still relies on public infrastructure investment. In looking at the future of Islamic finance I think it is first necessary to talk about the state of the Australian economy and how the Government is positioning Australia to be a regional financial centre. Last July, I gave the opening address to the Symposium on Islamic Banking and Finance, jointly hosted La Trobe University. It is gratifying to be invited to return and it's interesting to reflect on the progress in this important area of international finance in this time. The Assistant Treasurer also visited Deloitte's Islamic Finance Knowledge Centre in Bahrain and addressed a national roundtable of key figures from the Islamic finance industry in the Gulf region. Without this approach, the gap on financial inclusion will only widen or contribute to diminishing financial health. When I spoke at the Islamic finance symposium just 11 months ago, it was hard to imagine the growth in interest from all sides in this global phenomenon. Geographically, Australia is well positioned within the Asia Pacific region to expand already strong trade linkages with the region through the Islamic finance sector. Stay up-to-date with our press releases, upcoming events and news. If you are refinancing, the valuation on the property is ordered immediately after you are granted a Conditional Approval. We will order a valuation of the property once you have provided us with a valid contract of sale. We will send you a conditional approval which gives you an indication of how much finance we may provide you. The conditional approval is also subject to certain conditions which may include a satisfactory valuation that is conducted by an independent valuer. There are no significant commercial benefits or features of Islamic home loans that wouldn’t be offered with a non-Islamic-compliant loan. The unique circumstances surrounding an Islamic home loan and the limited size of the market can cause lenders to charge more compared to a typical home loan in the form of profit. Your lending institution may approve your circumstance beforehand, allowing you to immediately choose a home that is within the price range they agreed upon, thereby facilitating your application process. As the Islamic religion forbids borrowing money to be repaid with interest, Aaban approaches a local financial institution that provides alternative forms of lending. The lender conducts a preliminary assessment of Aaban's financial situation and issues a conditional letter of approval on behalf of the funder. “Islamic finance is largely about the philosophical side of things – it’s where Western banking meets Islamic banking.

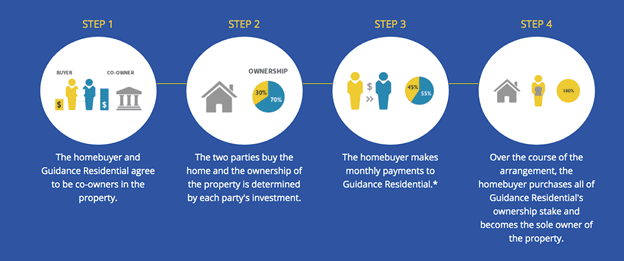

Islamic banking is just the tip of an ethical industry movement Mr Gillespie, a former retail banking executive with BankWest and Commonwealth Bank of Australia, says the bank will open up an entirely new market segment for Australia’s fast-growing Muslim population using best in class technology. The Assistant Treasurer, Senator the Hon Nick Sherry, has today held a series of talks with the international leadership of the Islamic finance regulatory and banking sectors. That’s where Islamic Bank Australia comes in, to offer Sharia-compliant options to those who want it. In Australia’s banking system, interest is implemented everywhere, making it difficult for the 3.2% of Australians identifying as Muslims to follow their own laws. NAB has cut fixed home loan interest rates for its four-year term to the lowest level in more than 20 years, giving borrowers value and certainty. If you encounter an error, please come back shortly and try again. This course provides a high-level insight into the architecture of Islamic finance. Current CSU students can view Subject Outlines for recent sessions. Please note that Subject Outlines and assessment tasks are updated each session. Hakan Ozyon, CEO and founder of Hejaz, spoke of the need to serve the huge, growing market of Muslims in Australia with Islamic finance. Michael Trist, formerly executive vice president at Dark Horse Capital, will join as general manager – sales and distribution. Target Market Determinations can be found on the provider's website. For more information please see Mozo's FSG, General advice disclaimer or Terms of use. Islamic Bank Australia (islamicbank.au) will be the first Australian bank to offer a full suite of retail and business banking services – all without interest and Shariah-compliant for the first time in Australia. The bank will first launch retail/personal banking with an everyday bank account, savings product (accounts that pay profit-share) and home finance (with co-ownership), before moving into business banking after a full licence is received. But, inclusion isn’t just about access, it’s also about experience. For security reasons please DO NOT provide any confidential or account specific information via email. Communications via email that are not encrypted are not secure. What you need to know as an MCCA customer, or more generally as a member of Australia’s Muslim community or the finance profession. System is currently experiencing issues and we are working on a solution. Visiting Manama, Bahrain on a visit to the Gulf, the Assistant Treasurer met with the Central Bank of Bahrain and key government economic and banking officials. 'Mozo sort order' refers to the initial sort order and is not intended in any way to imply that particular products are better than others. You can easily change the sort order of the products displayed on the page. The Australian Prudential Regulation Authority has officially authorised the first Australian Islamic bank to have a restricted deposit-taking license under the Banking Act. Get Halal Islamic Loans For Home, Car & Business Income could be an upfront commission and/or ongoing commission. The commission depends on the amount of the finance, cost of the product or other factors and may vary from product to product. Australia's Islamic bank offering Shariah-compliant banking services including everyday banking, savings products and home finance. We are a Restricted ADI, and are still building our systems and processes. Eventually, the asset is wholly paid off by the client and they own the house outright. You may approach any of the Islamic Bank Australia Islamic banking institutions listed above that offer Sharia-compliant products to know your options. Better still, you enlist the services of a mortgage broker who can best help you find a suitable financing. However, according to Ernst & Young, Islamic banking assets have experienced rapid growth and are forecast to increase by an average of 19.7% a year until 2018. A number of Australian financial institutions have examined Muslim financing concepts such as profit sharing and rent to buy while trying to avoid terms such as "interest" in contractual agreements. Driven by our Islamic values and ethos, our Shariah advisors ensure all our products are Shariah compliant. 'Mozo sort order' refers to the initial sort order and is not intended in any way to imply that particular products are better than others. You can easily change the sort order of the products displayed on the page. That’s where Islamic Bank Australia comes in, to offer Sharia-compliant options to those who want it. The Australian Prudential Regulation Authority has officially authorised the first Australian Islamic bank to have a restricted deposit-taking license under the Banking Act. We pay our respect to their Elders past and present and extend that respect to all Aboriginal and Torres Strait Islander peoples today. There is an explanation given to customers, and Aykan says the term is little more a formality. "What the MCCA has experienced, because the whole conventional system is based on the understanding of interest, is that our funders, our regulators, and whole heap of other bodies always use the word interest," says Aykan. Perhaps the largest issue, however, is the fact many Australian Muslims, while growing in number, see the traditional lending method with banks here to be both easier and cheaper. Dynamic asset allocation is ‘critical’ during times of economic uncertainty, according to a leading research and investment consultancy.... Mr Gillespie previously served as head of home loan distribution at the Commonwealth Bank and as head of mortgages at Bankwest. Your application is subject to the Provider’s terms, conditions and criteria. The prohibition on ambiguity often means that your provider will want to see very clear evidence that you can pay your mortgage and that you have a long history of sound financial management. You may find your deal more expensive due to the particular nature of Islamic mortgages and the fact that there aren’t many providers. Although you won’t be paying interest, you’ll be paying more than the selling price in the form of your rental or profit fee. Find out how much the rate is and what your eventual total repayment amount will be. How your loan to value ratio affects the amount you can borrow and how much your subsequent payments will be. Another financing company, Hejaz Financial Services, which is already in the home loan and superannuation space, says it has also just started the process of applying for a R-ADI. Murabaha financing is a method of Islamic financing commonly found in the Middle East and the Asian subcontinent. It occurs by way of a contract where an Islamic financier, upon the request of a customer, purchases an asset from a vendor and resells it to the customer with an agreed profit margin. The customer then makes periodic payments of an agreed amount over a set period of time. Depending on the financial institution, Islamic home loans may be slightly more expensive than non-Islamic home loans. However, this will depend on how the financial institution determines the profit made on the sale. In western culture, that has previously left Islamic businesses, people and investors at a disadvantage, but with major industry momentum in Islamic finance, it can now boost you forward. We use the guidance on national, international, and socio-economic issues outlined in Islamic code to help Australian Muslims to live and work accordingly while meeting and exceeding their business and financial goals. INSAAF exists to fulfil the increasing need for Muslim communities searching for financial solutions with experts in both areas to create an aligned result of equipment, vehicles or business success. During the Islamic loan term, the homebuyer continues to repay the borrowed amount and gains more and more equity in the property. They also continue to pay for the sole use of the home until they’ve repaid the loan and they own the property in full. Islamic Finance Halal Loans Sharia Finance Australia I believe Iskan Finance operates as an ethical business and we’re firm on NCCP compliance so people should take the comfort in the fact that we, and other providers, respect people’s rights under Australian law." None of the Islamic financing companies currently offering consumer finance products in Australia are licensed as fully fledged banks. That means that while they can offer home loans or super, they can't take deposits from customers. And at least two entities are seeking a licence to establish Islamic banks in Australia, alongside non-bank financial institutions that already offer sharia-compliant services. Islam prohibits interest from being charged on home loans. If you decide to apply for a credit product or loan, you will deal directly with a credit provider, and not with Canstar. Rates and product information should be confirmed with the relevant credit provider. For more information, read the credit provider’s key facts sheet and other applicable loan documentation for that product. This advice is general and has not taken into account your objectives, financial situation, or needs. Islamic home loans enable you to finance your property purchase with a different financial product that doesn't accrue interest in quite the same way. However, Australia’s credit laws still apply and the lender will still charge you for borrowing money. MCCA is Australia’s leading Shariah compliant finance and investments provider. Some Musharakah agreements involve diminishing partnership. The financier can provide knowledge and additional resources to the investor. They can lose money from the capital that they received or any additional investments they made. Someone who is unable to pay a debt through no fault of their own is penalized for it. Overall, very good customer service and will definitely recommend it. I have been with Amanah since March 2019 and so far their service has been superb from the beginning. Even during these challenging times their team are willing to help. Interest-based home loans that dominate our market generally allow people to borrow money from a bank, buy a house with that cash, and then pay the money back over a fixed term to the financier with interest. Our consultants are here to help you purchase your next property, vehicle or business asset without entering into an interest-based mortgage. Our Ijarah products can be tailored to suit individual and business needs. Let us guess, you’re here for Halal, and we have you covered. Hejaz wouldn’t exist if it wasn’t for Halal so it is our duty to provide you with authentic Sharia-compliant financial products and services. Featured Products and Advertisements are a form of advertising. But in the past decade, he has been taking out more Islamic loans, including one just a few months ago to expand his company's meat-processing ability. The complication in the Australian context is that laws aren't set up for this style of lending, so technically the home is owned by the household from the beginning, but with a legal agreement that the Islamic lender is entitled to it. Asad was an adviser to the Australian government's review of the taxation impact of Islamic finance in 2011. He's seen the sector grow but also battle to fit around Australia's banking framework. The head of local Islamic finance company Amanah Finance explains that the core philosophy goes further than avoiding interest. Ijarah Finance operates under the principle of Rent-To-Own otherwise known as Ijarah Muntahiya Bil Tamleek – A Lease Agreement with the option to own the leased asset at the end of the lease period. If the idea of owing your own property, vehicle or equipment via Ijarah appeals to you but you are currently paying off an existing mortgage we can help you replace it. Looking to make a change from the city life to the country life? If you are willing to make higher rental payments, lenders will often agree to let you make extra payments so you can become a homeowner sooner. Many existing compliant financing products give title to the customer, with a side contract specifying they’re buying it on behalf of the bank. The Dr Hewson-chaired company is part of the Crescent financial services group founded by former Australia Post director Talal Yassine. It is setting up two funds – an income fund that he expects to reach about $500 million in the next two to three years and a capital fund that will get up to about $200-$300 million in size. The bank has also invested in achieving the endorsement of Amanie Advisors, a global Shariah advisory firm, on behalf of its customers to provide comfort around the law compliancy while saving clients valuable time and money. “Many people that I speak to within the finance industry can’t comprehend how they are supposed to make money in banking without charging interest, but the example that I constantly share is to think of it in asset finance terms. NAB launches a first in Islamic business financing That's no doubt helped push them along while some of the major banks, especially in the U.S., have collapsed or needed billions of dollars in government funds after taking on too many bad loans. Founded in 1989, MCCA is the first and one of the leading providers of Islamic finance in Australia, a small but growing market. There's little competition other than a few others such as Sydney-based Iskan Home Finance. Join online and start your investment journey towards financial freedom. Take our quick Risk Profile Quiz to find the right investment product for you. A seminal book on Islamic finance by the world-renowned

0 Comments

Leave a Reply. |

ArchivesCategories |

RSS Feed

RSS Feed